Two countries, one flag

The monetary fracture that reveals the Argentina to come

Andy Spinelli | April 2026

It is six in the morning in Florencio Varela, on the southern outskirts of Buenos Aires. A woman lifts the shutter of the convenience store she has run for eleven years on a downtown corner. It is not raining but the sky is gray. She counts the coins in her cash drawer: three thousand pesos. Two months ago it was five thousand. It is not that she sells fewer snacks. It is that people increasingly pay by bank transfer and withdraw less and less cash. But the transfers take time. And the supplier who brings her cookies demands cash, because the supplier does not trust the pesos sitting in his own account either. She does not know what the transactional M2 is. She has not read the Facimex report. But she lives in her body what the economists in the Buenos Aires financial district describe with charts: people stopped wanting pesos.

Twelve hundred kilometers away, in Anelo, Neuquen, a drilling engineer has breakfast in the camp cafeteria. He is paid in pesos but converts them to dollars the same day he receives them. Not out of distrust: out of industry habit. Oil is priced in dollars, his bonus is calculated in dollars, his savings capacity is measured in dollars. Pesos are transit, not destination. Last month he bought a pickup truck in cash. He paid for it the same day he picked it up from the dealership. In Florencio Varela, the nearest dealership has six cars on the floor and two salespeople where there used to be eight.

These two scenes are reconstructions based on documented patterns, not individual testimonies. But they condense something the data confirms: Argentina is splitting into two economies that barely speak to each other anymore. And the number that certifies it has just been published: in March 2026, the demand for pesos fell to 7.6% of GDP, the lowest since the end of convertibility in 2002. The transactional M2 indicator, which measures cash in the hands of the public and demand deposits, sank 9% in real terms since December and 12.3% adjusted for seasonality. The consultancy Facimex describes it with clinical precision: it is not that there are more pesos than there should be. It is that nobody wants them.

What follows is not one more diagnosis. Argentina accumulates diagnoses the way it accumulates crises: one on top of another, none of them altering the course. What follows is an attempt to read this number, 7.6%, through three lenses that are rarely combined: the geopolitics of power, the strategic logic of actors, and the sociology of domination. And a question the reader can ask right now: of the pesos you earned this month, how many did you convert to dollars, how many did you leave in your account, how many did you spend before they lost value. That behavior multiplied by millions is the M2 collapsing.

I. The lens of power: who rescues a country nobody needs

Henry Kissinger would never ask who should rescue Argentina. He would ask why anyone would. And in that reformulation lies the first key to the problem.

Nations are not rescued out of solidarity. They are rescued when their collapse threatens an equilibrium that some power has an interest in preserving. It can be argued that Mexico in 1994 was rescued because its default would have dragged down the American banking system and the newly born NAFTA. Or that Greece in 2010 was rescued because its exit from the euro would have disintegrated the European political project. In each case, the rescue responded to a containment calculus, not an act of generosity.

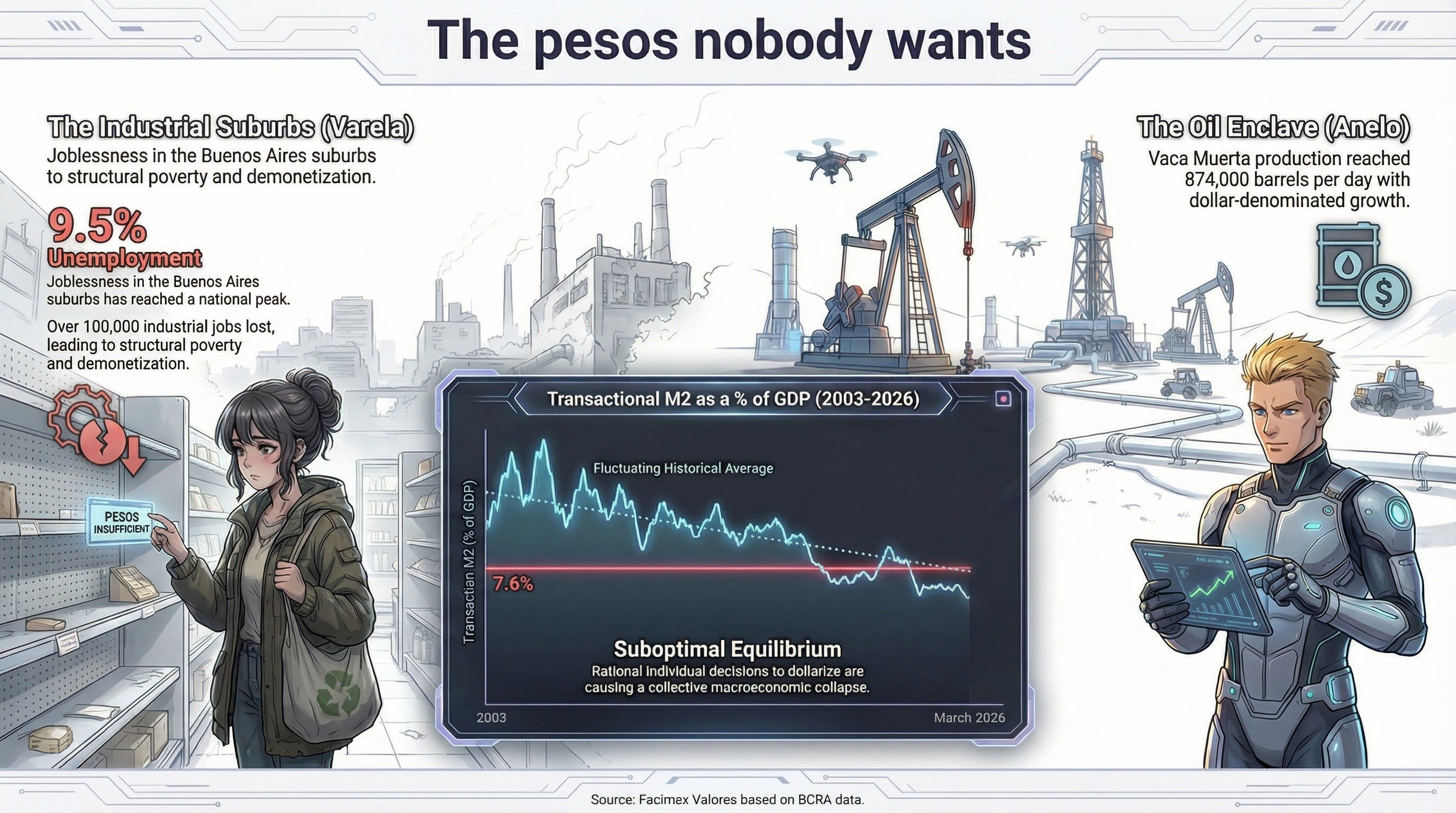

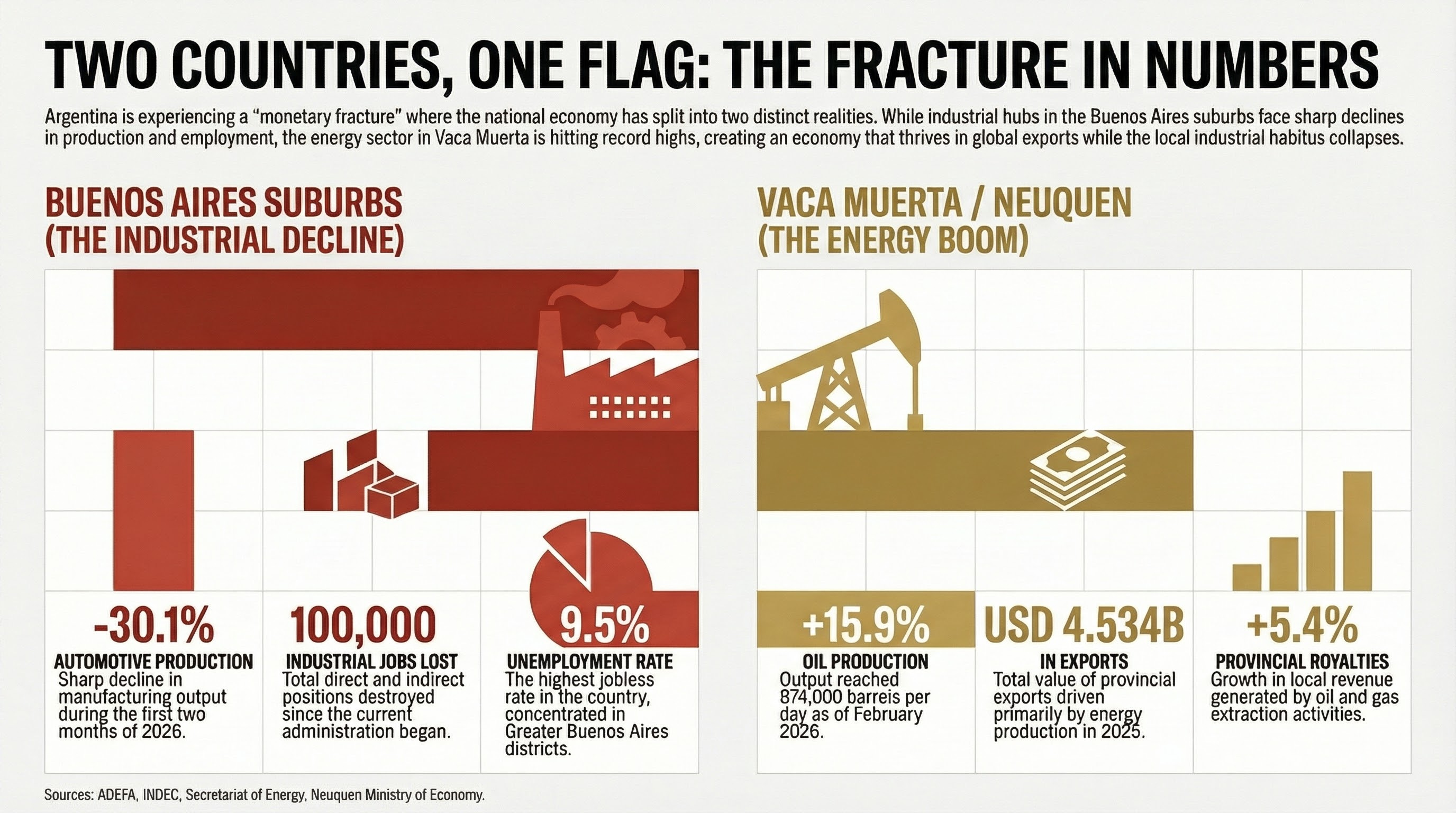

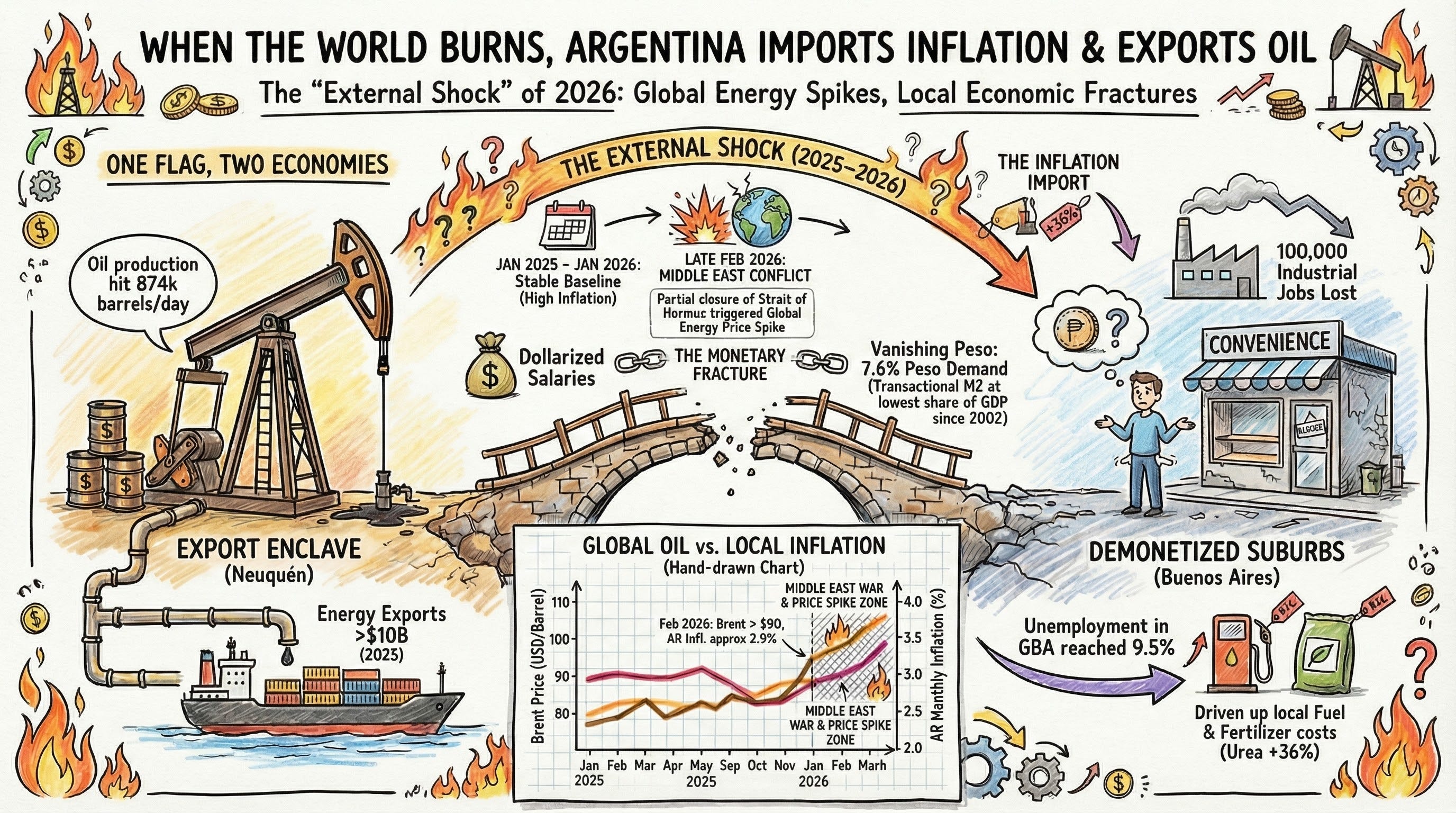

Argentina does not occupy that position. It is not systemically important to the global financial system. It does not control a resource whose interruption would paralyze supply chains. Its main exportable asset has historically been agricultural, and the global commodities market has substitutes. Vaca Muerta partially changes this equation: oil production reached 874,000 barrels per day in February 2026, a year-on-year increase of 15.9%, according to the Secretariat of Energy. Energy exports surpassed 10 billion dollars in 2025. And the Middle East war, which began in late February 2026 with the partial closure of the Strait of Hormuz, repositions Argentina as an alternative supplier outside conflict zones.

But Kissinger would draw a crucial distinction: being a convenient supplier is not the same as being an indispensable one. The United States is now a net energy exporter. Vaca Muerta interests Washington as a diversification piece for Europe and as a counterweight to Brazil’s gas dependency on Bolivia, but not enough to justify a second massive rescue. It is a second-tier asset on the global chessboard.

The Trump administration backed the IMF program of April 2025. It is plausible to interpret that this support included geopolitical alignment considerations: Milei positioned himself as Washington’s most visible ally in Latin America, anti-China, pro-Israel, willing to align on United Nations votes. If that reading is correct, the IMF package was, in Kissingerian terms, the price of loyalty. But loyalty has diminishing returns. If the monetary program fails, if inflation accumulates months of acceleration and the M2 collapses to historic lows, Washington faces the classic dilemma: double down or cut losses.

China watches with the calculus it applies in Africa and Southeast Asia: it does not rescue, it invests. And Chinese investment comes with conditions negotiated not in Congress but in opaque bilateral contracts. The currency swap with the PBOC remains active. The Patagonian dams are Chinese infrastructure on Argentine soil. The lithium of northwestern Argentina is a resource Beijing needs with existential urgency. An Argentine government cornered financially is, for China, the best negotiating opportunity.

The Kissingerian conclusion is cold: the country that needs to be rescued does not choose its savior. It is chosen by it. And when the negotiation comes, it will not be between Argentina and the international community. It will be between Washington and Beijing, using Buenos Aires as a piece on a board that Argentina does not control, did not design, and cannot exit.

II. The strategic lens: a game where everyone loses

John von Neumann, father of game theory, would have observed Argentina’s monetary crisis as a textbook case of suboptimal Nash equilibrium: every player acts rationally according to their individual interest, and the collective result is catastrophic.

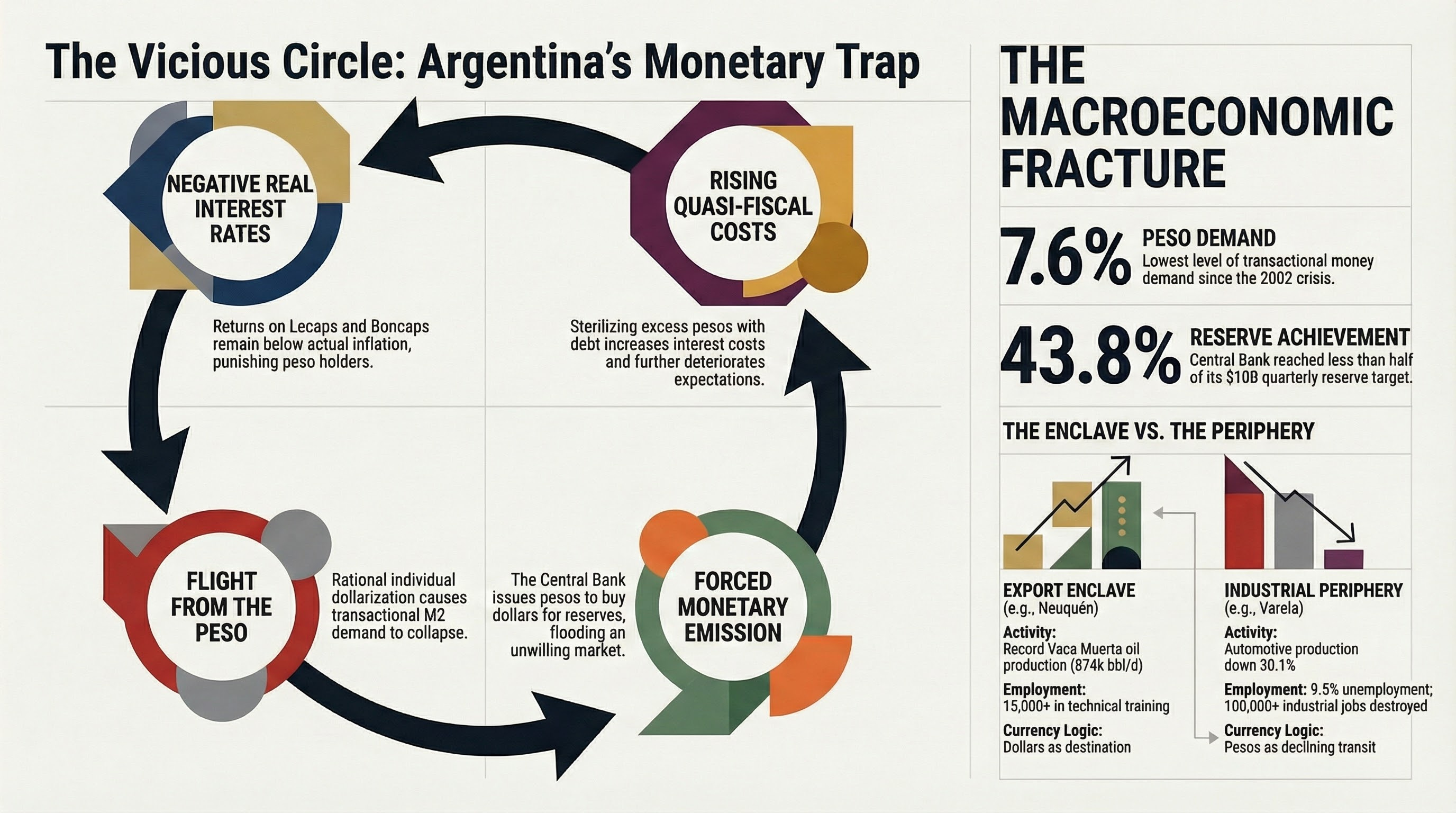

The saver who flees from the peso acts rationally. With accumulated inflation of 5.9% in January and February 2026 according to INDEC, and consultancies projecting a March CPI around 3% or more, holding pesos means paying an invisible tax. Real interest rates are negative: the overnight repo rate operates at an annual nominal rate of 21%, the effective monthly rates on Lecaps and Boncaps compressed to the 2% to 2.3% range, below actual inflation. The rational individual decision is to dollarize. But when millions make that decision simultaneously, peso demand collapses, exchange rate pressure rises, the Central Bank must sterilize with debt, and the inflation everyone was trying to dodge accelerates. It is a self-fulfilling prophecy at macroeconomic scale.

The Treasury managed to roll over nearly all its peso debt in the last March auction, but bank liquidity did not fall as expected. Parallel sources of injection offset the absorption: Central Bank dollar purchases, the reduction of reserve requirements from 50% to 45%, possible bond buybacks. Every player in the financial system optimizes their individual position, and the system as a whole oscillates without converging to a stable equilibrium.

Von Neumann would have identified the central problem: this is a game dominated by radical uncertainty. No actor knows how long the Middle East war will last, how many dollars the agricultural sector will actually liquidate during the heavy harvest of April through June, or what the true level of the Central Bank’s net reserves is. Agricultural companies liquidated 2.032 billion dollars in March, 57% more than in February, according to Bloomberg Linea. But the projection depends on factors no player controls. When uncertainty runs this deep, portfolio decisions become bets, and when bets become generalized, the system loses the ability to produce reliable price signals.

The Central Bank closed the first quarter with purchases of 4.386 billion dollars, barely 43.8% of the 10 billion dollar floor it had set as its 2026 target in its December 2025 communique. The remonetization plan envisioned raising the monetary base from 4.2% to 4.8% of GDP. But money demand, instead of recovering, collapsed. The game the Central Bank designed, buying dollars to remonetize without generating inflation, required an assumption that did not hold: that people would want the pesos that dollar purchases emit.

In game theory, this is called a dominated strategy that continues to be played because the player has no better alternative within the existing rules. The Central Bank cannot stop buying dollars because it needs to accumulate reserves. It cannot stop issuing because dollar purchases force it to. It cannot raise rates aggressively because it would increase Treasury debt costs and choke credit. It is trapped in an equilibrium it knows is suboptimal, but from which it cannot escape without changing the rules of the game.

III. The lens of domination: the capital that no longer circulates

Pierre Bourdieu would not have looked at the M2. He would have looked at what the M2 conceals: the social distribution of the capacity to play the economic game.

For Bourdieu, an economy is not an abstract market of rational agents. It is a field of forces where different actors possess different types of capital (economic, cultural, social, symbolic) and those capitals determine their position and their possibilities. What is happening in Argentina is a reconfiguration of the economic field that erodes the positions of those who only had industrial labor capital and consolidates those who possess financial capital or are embedded in globalized value chains.

The labor data is harsh. According to a report by the Atenas Group cited by specialized media, more than 100,000 direct and indirect industrial jobs have been destroyed since the start of the Milei administration. In Buenos Aires province alone, 46,000 formal positions disappeared, according to data from the provincial Ministry of Economy. Automotive production fell 30.1% in the first two months of 2026 according to ADEFA. Stellantis will eliminate a shift at its El Palomar plant starting in May. Unemployment in the Greater Buenos Aires districts reached 9.5% according to the INDEC household survey, the highest in the country.

On the other side of the field, Vaca Muerta produces 874,000 barrels per day. Neuquen exported 4.534 billion dollars in 2025, an 18.8% increase according to the INDEC provincial exports report. The Vaca Muerta Institute has surpassed 13,000 enrollees for technical training in drilling. Provincial royalties rose to 220.641 billion pesos in January 2026.

Bourdieu would call this naturalized symbolic violence: the destruction of industrial employment is presented as a necessary adjustment, an inevitable restructuring, a side effect of a model that works because it produces aggregate growth. GDP can grow from Vaca Muerta and mining while millions of people in the Buenos Aires suburbs see their standard of living decline. National accounts register growth. Everyday experience registers deterioration. Both are true at the same time.

Economist Martin Gonzalez Rozada, an adviser close to the administration, admitted it this week in El Cronista: provinces with mining, oil, and agricultural activity are recovering faster than the Buenos Aires suburbs. He even suggested that a population shift from the suburbs to the interior could occur. He said it with technical nonchalance. Bourdieu would have read it as the tacit acceptance that the economic model does not include millions of people, and that the implicit solution is for those people to move.

The Bourdiean dimension that nobody is discussing is that of the destroyed habitus. When a lathe operator in Quilmes loses his job and no reconversion path toward the growing sector exists, he does not only lose an income. He loses a set of dispositions, skills, social relationships, and labor identity that made him function in the economic field. The informality that absorbs those destroyed positions, the monotributo as refuge, precarity as norm: these are not transitions. They are social declassifications that tend to become structural.

And here the three lenses converge in a hypothesis that is mine, not Bourdieu’s: the destruction of industrial habitus may produce political apathy. If this speculation has substance, high electoral abstention would not be a statistical anomaly but the reflection of a population that lost the disposition to participate in the democratic game because it lost the economic position that made that participation relevant. A model that does not need an active electoral majority. It only needs the benefited minority to vote with intensity and the harmed majority to abstain. Proving this hypothesis would require crossing abstention data by industrial district with formal employment destruction data. That cross-tabulation does not yet exist. But the question deserves to be asked.

IV. What 7.6% reveals: two currencies in one territory

The fall in peso demand is not geographically homogeneous. In Neuquen, pesos circulate because there is activity, high dollar-denominated salaries that are converted to pesos for local consumption, investment. Provincial royalties rose to 220.641 billion pesos in January 2026. In Florencio Varela, pesos do not circulate because there is no activity to generate them. The national average transactional M2 conceals two completely different monetary economies: one that operates with dollarized enclave logic and another that is progressively demonetizing.

The trap is that monetary policy tools are national. The Central Bank’s interest rate is one. The exchange rate operates within bands updated with inflation since January 2026. Reserve requirements are uniform. There is no possibility of running expansionary monetary policy for the Buenos Aires suburbs and contractionary policy for Neuquen. Any adjustment the Central Bank makes to halt the fall in peso demand will disproportionately impact one or the other half of the country.

If it raises rates to retain pesos, it makes credit more expensive in the suburbs where there is already no credit. If it keeps rates low to avoid choking the suburbs, it accelerates the flight from pesos to dollars nationwide. The economic asymmetry produces a monetary policy asymmetry that has no technical solution within the current framework.

Facimex summarizes it precisely: a nominal anchor needs to be recovered to stabilize money demand. Translation: the IMF monetary program that replaced the crawling peg with M2 targets in April 2025 failed to anchor expectations. Inflation and expectations have risen consistently since then. And without a credible anchor, the floating exchange rate within bands becomes a pure exercise in credibility. Credibility is measured in exactly that: how many pesos people want to hold. 7.6% of GDP says very few.

Three different lenses converge on the same point. Kissinger shows that nobody will come to solve what Argentina does not solve on its own. Von Neumann shows that every rational actor produces a collective disaster because the rules of the game are broken. Bourdieu shows that the broken rules do not affect everyone equally: they destroy those already at the bottom and consolidate those already at the top. When a currency loses the confidence of its own population, when one sector of the country grows exporting to the world while another demonetizes in silence, when the tools of economic policy cannot govern the fracture, the problem has ceased to be technical. It is civilizational.

V. What comes next: a warning for the weeks ahead

March inflation data will be released on April 14. Consultancies project between 2.8% and 3.5%. If it confirms the acceleration, it will mark multiple consecutive months of rising inflation. With negative real rates, peso demand at historic lows, and Brent above 100 dollars per barrel pushing up fuel and fertilizer costs (urea rose 36% in three weeks according to the Argentine Rural Society, local diesel 22%), the combination is explosive.

The heavy harvest enters liquidation between April and June. If agricultural companies liquidate at a strong pace, the dollar supply will partially relieve exchange rate pressure. But every dollar the Central Bank buys will issue pesos that nobody wants. Without an expectations anchor, those pesos will flow directly to the parallel exchange rate or to dollarized goods. The spread can widen. Inflation can jump.

The OECD just revised its projections: GDP growth cut to 2.8% for 2026, inflation adjusted to 31.3% (13.7 points above its December estimate). The IMF is watching. If money demand continues to fall, the basic assumption of the program is refuted by the evidence. What follows is a waiver with target renegotiation or a suspension of disbursements. Both options are politically lethal.

Meanwhile, automotive production fell 30.1% in the first two months according to ADEFA. Stellantis eliminates a shift in May. Every factory that adjusts drags down its suppliers, its truckers, the shops on the block. The 9.5% unemployment rate in the suburbs is the easy indicator. The hard indicator is inactivity: people who stopped looking for work. That is the poverty that becomes structure.

If in the coming weeks there is no clear signal of a course change (a rate that stops the peso hemorrhage, a productive integration program that connects the two economies, a credible fiscal signal that is not more austerity on those who have nothing left to cut), the scenario converges toward what every Argentine monetary crisis produces when left to mature: a disruptive exchange rate event that liquidates in hours what accumulated over months.

Argentina has a window today. The Middle East war is driving up the price of the oil it exports. The heavy harvest promises fresh dollars. Vaca Muerta is consolidating records. These assets exist. The question is whether they will serve to build a bridge between the country’s two economies or whether they will be captured by enclave logic while the suburbs sink. There is not much time to decide.

VI. Two countries, one decision

I return to the woman at the convenience store in Florencio Varela. When she lifts the shutter tomorrow at six, she will not know that the transactional M2 is at 7.6% of GDP. She will not know that Facimex diagnosed a collapse in peso demand. She will not know that the OECD cut Argentina’s growth projections. What she will know is that she has three thousand pesos in the drawer and yesterday she had four thousand. What she will feel is that pesos weigh less in her hand every day.

Twelve hundred kilometers away, the engineer will collect his paycheck and convert it to dollars. He will not even think about it. It is automatic. Like breathing.

These two scenes are the same Argentina. The difference is that one of them has a visible future and the other is losing its present. The decision to connect them or let them diverge is not technical: it is political, it is moral. Prebisch described it in 1949 with the center-periphery structure. Only now the center and the periphery coexist within the same territory, share the same currency that one uses and the other discards, vote for the same president, and walk in opposite directions.

The Argentina that is coming is not decided in the markets. It is decided in whether there is political will to build the bridge between Anelo and Florencio Varela before the distance becomes irreversible. The 7.6% clock is already ticking.

___

References

ADEFA (2026, March). Automotive production report, first two months 2026. Argentine Automobile Manufacturers Association. https://www.adefa.org.ar/

BCRA (2025, December 18). Deepening of the monetary aggregates framework: remonetization phase 2026. Central Bank of Argentina. https://www.bcra.gob.ar/politica-monetaria/

BCRA (2026, March). Market Expectations Survey (REM), February 2026. Central Bank of Argentina. https://www.bcra.gob.ar/relevamiento-expectativas-mercado-rem/

Bloomberg Linea (2026, April 1). Argentine agricultural dollar inflows normalize ahead of heavy harvest. https://www.bloomberglinea.com/

Bourdieu, P. (1979). La distinction: critique sociale du jugement. Les Editions de Minuit.

Bourdieu, P. (2000). Las estructuras sociales de la economia. Anagrama.

El Cronista (2026, April 1). From the suburbs to the interior: the labor exodus anticipated by trade opening. https://www.cronista.com/

Facimex Valores (2026, April). Money demand report: Private Transactional M2 at lows since convertibility.

Grupo Atenas / Pollera, M. and Macchioli, M. (2026, March). Report on industrial employment destruction.

INDEC (2026, February). Consumer Price Index (CPI), January 2026. https://www.indec.gob.ar/

INDEC (2026, March). Consumer Price Index (CPI), February 2026. https://www.indec.gob.ar/

INDEC (2026, February). Industrial capacity utilization, January 2026. https://www.indec.gob.ar/

INDEC (2026). Permanent Household Survey (EPH), Q4 2025.

INDEC (2026). Provincial Origin of Exports (OPEX), 2025. https://www.indec.gob.ar/

Infobae (2026, April 2). Oil production remained at record levels in February driven by the Vaca Muerta boom. https://www.infobae.com/

Infobae (2026, March 26). OECD cuts Argentina growth forecast to 2.8% in 2026. https://www.infobae.com/

Kissinger, H. (1994). Diplomacy. Simon and Schuster.

Kissinger, H. (2014). World Order. Penguin Press.

Ministry of Economy, Buenos Aires Province / Lopez, P. (2026, March 31). Provincial industrial production data, February 2026 [X post].

Nash, J. (1950). Equilibrium points in n-person games. Proceedings of the National Academy of Sciences, 36(1), 48-49.

Neumann, J. von, and Morgenstern, O. (1944). Theory of Games and Economic Behavior. Princeton University Press.

OECD (2026, March). OECD Interim Economic Outlook, March 2026. https://www.oecd.org/

Prebisch, R. (1949). The economic development of Latin America and some of its principal problems. ECLAC.

Rial, S. (2026, April 2). Peso demand at concerning levels. Ambito Financiero. https://www.ambito.com/

Secretariat of Energy (2026). Oil and gas production data, January-February 2026. https://www.argentina.gob.ar/economia/energia/

Argentine Rural Society (2026, March). Impact of the Middle East conflict on agricultural production costs.

Stellantis Argentina (2026, March). Statement on El Palomar plant production adjustment [Press release].